M&A Critique is the only magazine, published from India which gives News, Deals and Analysis of Merger & Acquisitions, Restructuring, Takeovers and Joint Ventures. M&A Critique gives unique insights and expert’s critique on middle market deals, Corporate Strategy for inorganic growth, Case study of deals, M&A Happenings in the High Court, M&A Digest, Legal insights and updates on the subject, content on leadership and much more.

Binani Cement in UltraTech Cement’s Shelf

Get link

Facebook

X

Pinterest

Email

Other Apps

Binani Cement Limited (BCL) is the flagship subsidiary of Binani Industries Limited (BIL), representing the Braj Binani Group. BCL has a capacity of 8.55 MTPA which includes an integrated cement unit with capacity of 4.85 MTPA and a split grinding unit with capacity of 1.4 MTPA in the State of Rajasthan. BCL has investments in subsidiaries in China and UAE. Total revenue of Binani cement for Mar-17 was ₹1,534.62 crores and a reported loss of ₹347.60 crores for that year. The company went under the insolvency resolution process initiated by its financial creditor in July 2017 with finally a resolution plan accepted in Nov 18 by NCLAT without any haircut to financial and operational creditors.

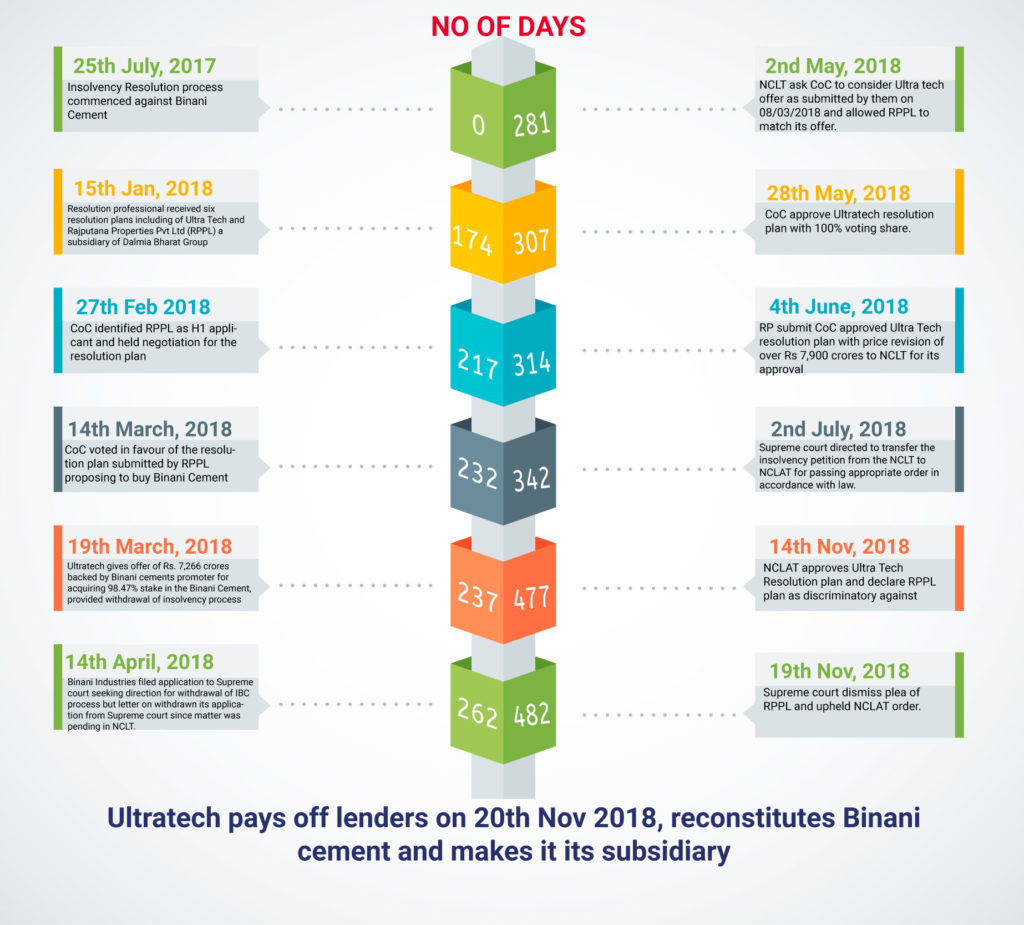

Corporate Insolvency Resolution Process (CIRP)

On 25thJuly 2017, NCLT accepted an application filed by Bank of Baroda one of the financial creditors for initiation of Corporate Insolvency Resolution Process (CIRP) against the company. After various legal hurdles and multiple applications challenging resolution plan, finally on 14thNovember, 2018, NCLAT approved the resolution plan as submitted by Ultratech for Binani Cement and further Supreme Court also upheld NCLAT order.

CIRP Journey

Resolution plan:

As per Ultra tech resolution plan, all creditors, financial as well as operational creditors (other than related party) are getting 100% of their claims amount, further financial creditors are also paid interest amount accrued during the CIRP process which was never considered before in any other resolution plan.

Comparison between RPPL and Ultra Tech Payment offers to creditors of Binani Cement

Table 1: Claims and Resolutions (All Figs in ₹ Crores)

Particular

Claim amount

Proposed payment by RPPL

Proposed payment by Ultratech*

CIRP cost

132

132

134**

Financial creditors with direct exposure to corporate debtor

4,042

4,041

4,359

Financial creditors to whom corporate debtor was a guarantor

2,428

2,225

2,493

Operational creditors (other than workmen)

676

184#

616#

Equity/Working Capital Infusion

-

350

350

Total

7,283

6,932

7,951

*include interest on financial creditors debt till 30/04/2018

**includes claims not approved by CoC

#Related parties dues are paid Nil.

What was not right in RPPL resolution plan

RPPL in its resolution plan has given preferential treatment to different creditors within same class of creditors by paying lesser amount to few creditors in comparison with others which was objected before adjudicating authority and went against them.

Further Exim Bank submitted before Adjudication Authority that they were forced to vote favour of the ‘Resolution Plan’ as the ‘Resolution Applicant’ (‘RPPL’) in its plan made it clear that those who will not vote in favour of its ‘Resolution Plan’ will be paid liquidation value which is almost Nil.

Payment to operational creditors are also not on same parameters like trade creditors with Outstanding (O/s) less than Rs 1 crore are paid 100% of verified claims, trade creditors with O/s 1-5 crores are paid 40% or 1 crore whichever is higher and trade creditors with O/s 5-10 crore are paid 25% or 2 crore whichever is higher, such preferential treatment is not there in IBC.

Table 2: Financial & Operational Creditors

Category

Proposed Amount(Rs. In Crores)

Percentage payment wrt to claims

Financial Creditors to whom corporate debtor was a guarantor

State Bank of India (Hong Kong)

3.7

10%

Export-Import Bank of India

450

72.59%

All other banks (Except EXIM Bank & SBI-Hong Kong branch)

1,771

100%

Operational Creditors (Other than workmen)

Unrelated Parties

151

35%

Statutory Liabilities

33.10

19.3%

Valuation of Binani Cement:

Liquidation value as ascertained during CIRP process was Rs 2,300 crores whereas the winning bid was almost 4 times of it, which shows valuation was way below its potential. Ultratech will finance the Binani acquisition of Rs 7900 crores with 60% debts and 40% from equity.

Ultratech’s interests in Acquisition

Ready to use assets which are currently operating at 50% capacity utilization

Location benefit since Binani cement unit is in Rajasthan which will help Ultratech realignment of its existing market for Rajasthan and Gujarat.

Ultra tech cement sells more than 2.5 MT per month in North + West markets and with Volume addition by 5-6% on existing base, will meet the growing demand and make them one of the strongest in Northern Indian market.

Alignment of Binani cement dealer networks with Ultratech’s market strategy

Acquisition provides access to large limestone reserves enough for another 5MTPA capacity addition with combined reserve life of 35-40 yrs.

Access to Thermal power plan of 70MW of Binani cement

Table 3: Past Acquisitions by Ultratech Cement

Target

Year

Capacity (MTPA)

Value (EV) (Rs in crores)

EV /MTPA

Star Cement

2011

3

1,754

584.67

Gujarat Unit of Jaypee Group

2013

4.8

3,800

791.67

Jaiprakash Associates Limited

2016

21.2

16,189

763.63

Century Textile (Cement Business)

2018

13.4

8,138

607.31

Binani Cement - current cement capacity

2018

8.55

7,951

929.98

With likely brownfield expansion of 5 MTPA

13.55

9,547

704.54

RPPL Interests in Binani cement

Dalmia Bharat, holding company of RPPL has significant presence in southern & eastern market and acquisition of Binani cement would have given them Northern India market along with a running plant

Resolution plans from other stakeholders point of view:

For Creditors: Financial and operational creditors are getting 100% of their claim value and further financial creditors are also getting interest during CIRP period.

For Binani cement shareholders: They loose control of the company and not received any penny from the plan.

Conclusion

Binani Cement clearly was having problems, squeezed for working capital and unable to generate free cash flow. Furthermore, cement industry is seeing consolidation from the past years which makes it difficult to standalone and create and maintain its brand to generate profits in the future. Submission of the company into InsolvencyProcess, was a God-sent opportunity for Ultratech to strengthen its presence in the North-Western market.

Ultratech got assets at competitive rate while repaying outstanding credits of all stakeholders including suppliers customers and employees, only party affected and lost is non-promotor shareholders. Although subjective, resolution plan should provide some compensation to non-promotor shareholders, more so in this case.

Binani cement Insolvency resolution case is considered as one landmark achievement of Insolvency & Bankruptcy Code as assets will be quickly put to use to generate returns for all concerned and generate tax revenues for the government.

Hindustan Unilever outruns Nestle and bags GSK’s nutrition business in its kitty. This being the country’s biggest consumer goods deal is an all equity deal. Hindustan Unilever Ltd (HUL) , incorporated in 1933 and is a subsidiary of Unilever, one of the world's leading suppliers of Food, Home Care, Personal Care and Refreshment products. Unilever has over 67% shareholding in HUL. HUL is India's largest fast-moving consumer goods company with a heritage of over 80 years in India. HUL operates in four business segments, they are: Personal care includes products in the categories of oral care skin care, soaps, hair care, talcum powder and colour cosmetics. Home Care includes detergent bars detergent powders Foods & Refreshments Water purifier called Pureit The shares of HUL are listed on BSE and NSE and current market cap is ~₹3,86,076 Crores. GlaxoSmithKline Consumer Healthcare Ltd (GSK), is one of the largest players in the Health Food Drinks industry in India...

HAL Offshore Ltd (HAL) is an unlisted public company, part of Delhi based MM group and a leading ‘End to End’ solution provider of underwater services and EPC services to the Indian Oil and Gas Industry catering complete need of both offshore and Onshore requirements. The company has two distinct businesses viz., EPC & Vessel Division and Investment Division (consist of investment in real estate, shares and other securities), major clients being ONGC, Oil India and Cairns. Having a Networth of Rs 216.93 crores as on June 30, 2017. Seamec Ltd is a listed public company and a subsidiary of HAL offshore, one of the largest provider of diving support vessel in the Asia Pacific region, has experience in the ongoing subsea inspection, repair, maintenance and light construction required for the efficient and productive support of offshore oil production. The Company has a market cap of Rs 452 crores, shares are listed on BSE and on NSE. Transaction HAL offshore will demerge it...

Alembic Ltd (Alembic), incorporated in 1907, is part of Alembic group and it is engaged in the business of manufacturing and trading active pharmaceutical ingredients (API) and Real Estate Developments. It also has investment in Alembic Pharmaceuticals Limited (APL). Shreno Limited (Shreno), incorporated in 1944, is engaged in the business of manufacturing and trading of glassware items, machinery and equipments (engineering) required for various industries, making investments and real estate developments. Nirayu Pvt. Ltd. (Nirayu), incorporated in 1971, is currently holding investment in shares and securities of various entities. Current Shareholding of the companies Please Note: 1% OCPS of Shreno limited of book value Rs. 8.71 crores were converted in equity shares by alembic Limited in FY 2018 Therefore the final total investment by Alembic in equity is Rs. 35.13 crores. Alembic acquired 55% stake in Alembic City Limited resulting into WOS of the company ...

Comments

Post a Comment