M&A Critique is the only magazine, published from India which gives News, Deals and Analysis of Merger & Acquisitions, Restructuring, Takeovers and Joint Ventures. M&A Critique gives unique insights and expert’s critique on middle market deals, Corporate Strategy for inorganic growth, Case study of deals, M&A Happenings in the High Court, M&A Digest, Legal insights and updates on the subject, content on leadership and much more.

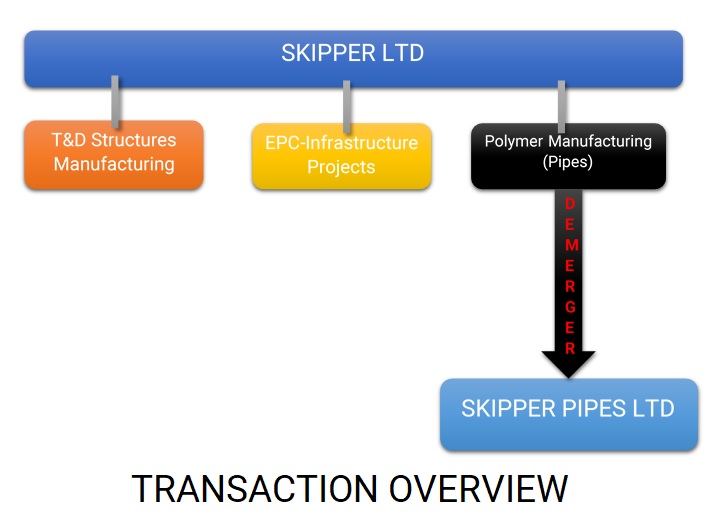

SKIPPER DEMERGES POLYMER BUSINESS FOR POTENTIAL GROWTH

Get link

Facebook

X

Pinterest

Email

Other Apps

Skipper Limited (Skipper), incorporated in 1981, is the largest manufacturer of Transmission & Distribution Structures in India with engineering and manufacturing facilities in Eastern India. The company takes advantage of the available power and steel supply, the cost-effective labour, and proximity to ports. It has four state-of-the-art manufacturing plants in this region, two in Jangalpur; one in Uluberia near Kolkata, West Bengal; and one in Palasbari, near Guwahati). The Guwahati plant commenced operations in March 2017 and aims to tap the growing demand for T&D products in the North East region. The total installed capacity of Engineering products now stands at 265,000 MT.

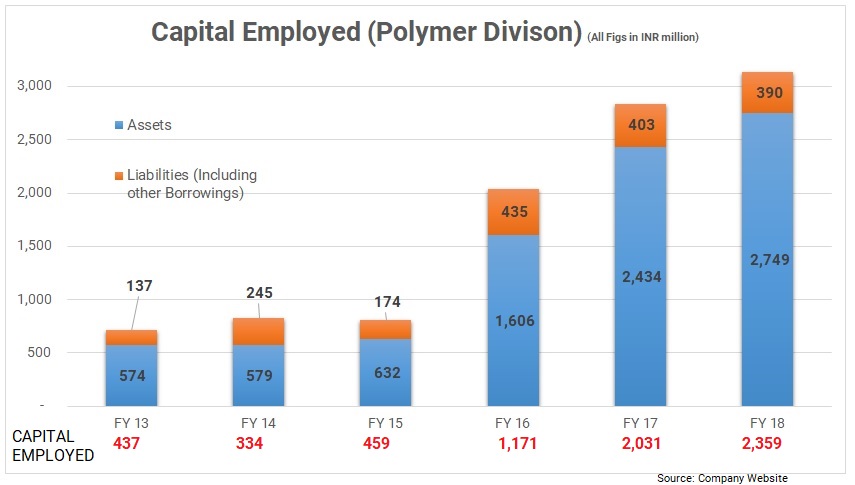

The company’s Polymer Product Segment has a manufacturing capacity of 51,000 MTPA. Over 70% of the gross block is less than six years old, and Skipper is one of the very few companies in India to be assured of CPVC for the manufacture of state-of-the-art pipes. Skipper is the only Company in the sector to undertake an asset-light route for expansion, setting up satellite manufacturing units to cater to the different zones of the country.

TRANSACTION

Demerger of Polymer products division/undertaking of Skipper Limited in Skipper Pipes Limited (SPL) except palasbari unit situated at Guwahati Assam with Appointed Date as 1St April 2018 Swap Ratio is 1:1 as Mirror Image of Skipper Limited.

Please Note:

Skipper Pipes is currently owned by the promoters with no business. As part of scheme of merger, the shares held by promoters in SPL will be cancelled which will maintain mirror image shareholding post demerger.

Demerger include joint venture entity with Israel based Metzerplas for drip irrigations solutions in India

RATIONALE

Polymer products has significant growth potential and require management separate to focus

Attracting different set of investor, strategic partners, Lenders, and other stakeholders

Develop their own network of alliances and talent models that critical to success

High Degree of independence as well as accountability with autonomy for each business segment

Current Shareholders the ability to continue to remain invested in both or either of the two companies giving them greater flexibility in managing and/or dealing with their investments

VALUATION

Since the shareholders of Sipper shall have the same percentage of stake, ownership, control, and voting rights in Skipper and SPL and accordingly valuation of the companies has not been arrived. However, the post-demerger is to unlock the value for Engineering and manufacture of transmission and distribution structure and to attract investors which are focused on initial phase of business for Polymer products business.

TAXATION

Since it is compliant demerger there will be no tax implication in the hands of the shareholders and the company.

DEMERGED UNDERTAKING

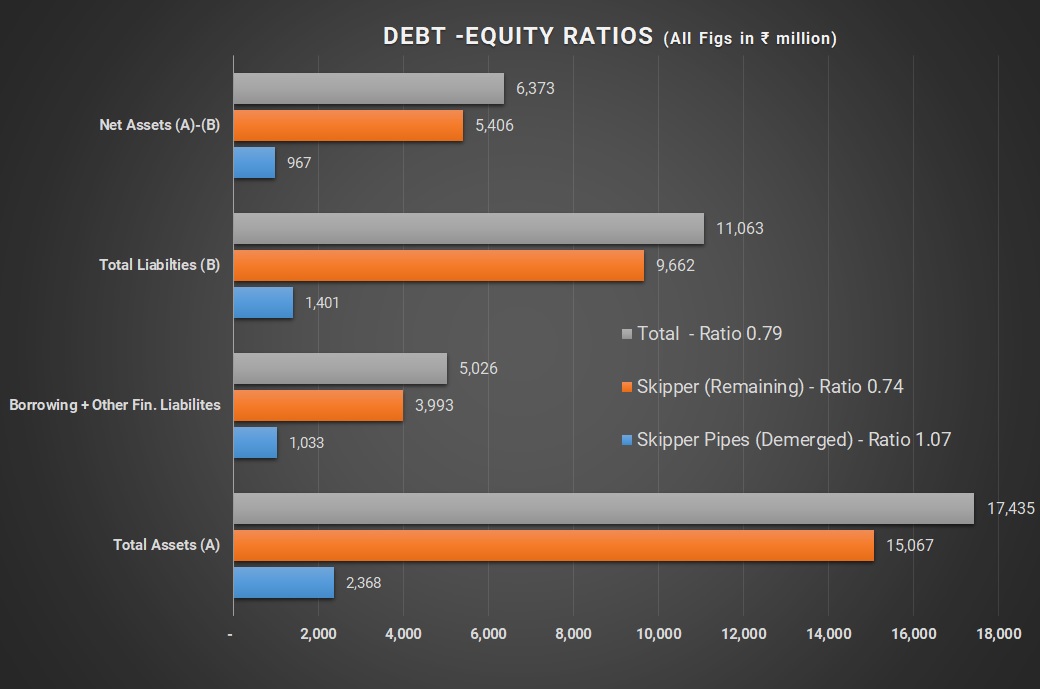

The Net assets of the Undertaking as on appointed date is as mentioned below. However, the debt-equity ratio of demerged undertaking is higher as major expansion is done in last 5 years.

The net worth of the demerged undertaking as on 31.03.2018 is Rs. 967.08Mn. However, the company has infused in the last 6 years approx. Rs. 1921.64 Mn in Demerged Undertaking. The management is positive for expansion to increase capacity to 1,00,000 MTPA. Currently, the Demerged Undertaking is at break even for cash positive. However, for remaining undertaking post demerger it will reflect improved profit margin.

Table 1: Financials of Skipper and Skipper Pipes (All Figs in ₹ Millions)

Particulars

Demerged Undertaking

Remaining Undertaking

Total(FY 2018)

Revenue

2,148.93

18,927

21,076.18

Profit before Depreciation, Interest & Unallocated Exp.

224.43

3,141

3365.93

Depreciation

-73.50

-386

-459.06

Interest Expenses

-161

-623

-784.45

Unallocated

-34

-298

-331.98

Interest Income

-

13

13.45

PBT

-44.16

1,848.05

1,803.89

Tax

-

628

626.27

PAT

-44

1,220

1177.62

Cash Profit

29.35

1,605.27

1,636.68

PAT Margin

-2.05%

6.44%

5.59%

No. of Shares

102.67

102.67

102.67

EPS

-0.43

11.88

11.47

STRATEGY

The company’s strategy being polymer business, started as a sustainable business. Now polymer business is matured enough to generate its own cash flow and/or the management may want to invite strategic partner for future expansion. The consolidated entity had much benefits in terms of taxation as polymer was not profit making and it will have ceased to exist. However, the equity capital for polymer business might be higher as it will not be able to in the initial phase of expansion, so the management thought of lower swap ratio to maintain lower capital.

CONCLUSION

The transaction of demerger is to unlock the value for transmission and distribution structure business which is cash positive and profit division whereas to create another listed company to attract difference set of investors or strategic partner for polymer products business which is in initial phase of growth.

Hindustan Unilever outruns Nestle and bags GSK’s nutrition business in its kitty. This being the country’s biggest consumer goods deal is an all equity deal. Hindustan Unilever Ltd (HUL) , incorporated in 1933 and is a subsidiary of Unilever, one of the world's leading suppliers of Food, Home Care, Personal Care and Refreshment products. Unilever has over 67% shareholding in HUL. HUL is India's largest fast-moving consumer goods company with a heritage of over 80 years in India. HUL operates in four business segments, they are: Personal care includes products in the categories of oral care skin care, soaps, hair care, talcum powder and colour cosmetics. Home Care includes detergent bars detergent powders Foods & Refreshments Water purifier called Pureit The shares of HUL are listed on BSE and NSE and current market cap is ~₹3,86,076 Crores. GlaxoSmithKline Consumer Healthcare Ltd (GSK), is one of the largest players in the Health Food Drinks industry in India...

HAL Offshore Ltd (HAL) is an unlisted public company, part of Delhi based MM group and a leading ‘End to End’ solution provider of underwater services and EPC services to the Indian Oil and Gas Industry catering complete need of both offshore and Onshore requirements. The company has two distinct businesses viz., EPC & Vessel Division and Investment Division (consist of investment in real estate, shares and other securities), major clients being ONGC, Oil India and Cairns. Having a Networth of Rs 216.93 crores as on June 30, 2017. Seamec Ltd is a listed public company and a subsidiary of HAL offshore, one of the largest provider of diving support vessel in the Asia Pacific region, has experience in the ongoing subsea inspection, repair, maintenance and light construction required for the efficient and productive support of offshore oil production. The Company has a market cap of Rs 452 crores, shares are listed on BSE and on NSE. Transaction HAL offshore will demerge it...

Alembic Ltd (Alembic), incorporated in 1907, is part of Alembic group and it is engaged in the business of manufacturing and trading active pharmaceutical ingredients (API) and Real Estate Developments. It also has investment in Alembic Pharmaceuticals Limited (APL). Shreno Limited (Shreno), incorporated in 1944, is engaged in the business of manufacturing and trading of glassware items, machinery and equipments (engineering) required for various industries, making investments and real estate developments. Nirayu Pvt. Ltd. (Nirayu), incorporated in 1971, is currently holding investment in shares and securities of various entities. Current Shareholding of the companies Please Note: 1% OCPS of Shreno limited of book value Rs. 8.71 crores were converted in equity shares by alembic Limited in FY 2018 Therefore the final total investment by Alembic in equity is Rs. 35.13 crores. Alembic acquired 55% stake in Alembic City Limited resulting into WOS of the company ...

Comments

Post a Comment